Could the war with Iran keep inflation higher for longer?

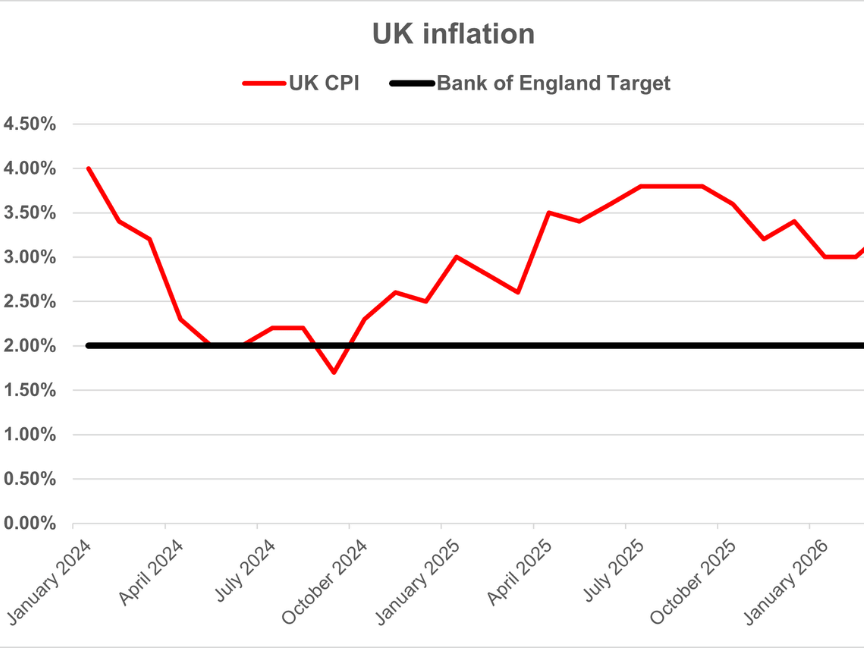

When the Bank of England met in early February of this year, the summary of the meeting said, “Although above the 2% target currently, consumer price index (CPI) inflation is expected to fall back to around the target from April, owing to developments in energy prices, including from Budget 2025.”

The reference to energy prices had nothing to do with the focus of current interest: oil. The Bank was looking forward to the reduction in the domestic energy price cap from 1 April. That was set in train by the Chancellor’s decision in last November’s Budget to transfer some renewable energy costs from bills to general taxation for three years.

At the time, the move by Rachel Reeves was seen as having three benefits. It would:

- reduce the average annual utility bill by £150 (all other things being equal);

- lower inflation, providing some good economic news; and

- feed through lower government borrowing costs, some of which are linked to inflation.

Less than four weeks after the Bank of England had mused about inflation finally reaching the target set for it by the Chancellor, the Iran war began. Brent Crude, one of the oil price benchmarks, rose from around $70 a barrel in late February to over $110 a month later, before settling around $100 (at the time of writing).

The UK’s March inflation figures showed the first impact of the oil price jump, with annual inflation rising from 3.0% to 3.3%. The detailed data showed overall motor fuel prices rising by 4.9% in the year to March 2026, compared with a fall of 4.6% in the year to February. The March fuel inflation figure was the highest recorded since January 2023. There is probably more pain to come as the fuel prices were based on the average across March, which were 140.2p a litre for unleaded and 158.7p for diesel.

So far, there are no forecasts that inflation will return to the 10%+ of 2022/23. However, for the second time in less than five years, we have all been reminded that inflation has not disappeared and cannot be ignored.

Get in touch with us by calling 0114 266 4432 or email info@smh.group for more information.

Comments are closed.