Investment markets reacted sharply to Donald Trump’s Iran ‘excursion’ in March, with oil prices, equities and bond yields all experiencing short-term volatility as events unfolded.

However, when looking at the quarter as a whole, the overall movement was more measured than the headlines might suggest, with markets showing resilience as initial shocks began to settle.

2025 was a strong year for investment markets, with the UK delivering a particularly notable performance. The FTSE 100 rose by more than 20% over the year, outperforming both Europe and the US when measured in local currency terms.

This positive momentum carried into the start of 2026. Expectations were that interest rates would continue to ease across many economies, while inflation, although still present, was no longer seen as a major concern.

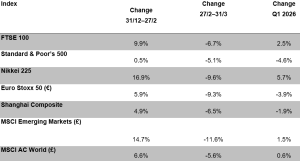

By Friday 27 February, as shown in the table above, most markets were trading above their closing levels for 2025.

Japan stood out as the strongest performer during this period, supported by market confidence following the snap election victory of new Prime Minister Sanae Takaichi.

Then, on 28 February, the US-Israel war with Iran started.

For several months, the US had been building what Donald Trump labelled ‘an armada’ in the seas around Iran, action which prompted a rise in the oil price to a little over $70 a barrel. However, the timing of the attack was a surprise, which deeply unsettled investment markets, as was evident when trading resumed on Monday 2 March. The remainder of the month was a largely downward path, interrupted by brief rallies when it appeared that a decisive change of mind by Trump might prevail. By the end of March and the first quarter, with oil over $100 a barrel, a clean resolution looked unlikely.

Stand back a little and look at investment markets’ performance across the quarter and the picture is not quite as you might imagine:

- While equity markets fell in March, the falls were mostly matched by the increases in January and February. If you are one of those people who only look at quarterly valuations, you might not even register the ‘exciting’ three months that have passed.

- Gold, the classic safe haven, investment, proved anything but. Its dollar price fell by 10.3% in March, although over the quarter it gained 7.7%.

- Arguably, the rise in oil prices had the greatest effect on government bond markets, as bond investors loathe inflation. The UK gilts market was among the hardest hit, which bodes ill for a government that plans to borrow over £250 billion in 2026/27.

The first quarter of 2026 has provided plenty of noise – and a reminder that the short-term cacophony can be just a little deafening.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

For more guidance and support in naviagting financial markets, talk to a member of SMH’s team. Give us a call at 01142 664 432 or email info@smh.group for more information.

Comments are closed.